By Dr. A.K. Garg, Scientist ‘F’, MeitY, [email protected] and Ms. Sangeeta Hemrajani, Sc ‘D’, STPI Noida, posted at MeitY, [email protected]

During inauguration of Digital India Week 4th – 9th July 2022, our Hon’ble Prime Minister of India stated that “Fintech is indeed the best technology for the people, of the people and by the people.

The technology used in this is developed by Indians i.e. ‘by the people’. We have made this technology a part of our life i.e. ‘of the people’. It has simplified the lives ‘for the people’.”

1. Let’s look at some statistics about the Growth of Indian Fintech start-ups and its potential

- According to Niti Aayog, India is one of the fastest growing fintech markets globally and industry research has projected that $1 trillion will be digitally disbursed by 2029. The Indian Fintech ecosystem is the 3rd largest in the world attracting nearly $6 billion in investments since 2014. [1]

- India made 7,422 crores digital payments transactions in FY22 at 33% growth rate (YoY) as per Ministry of Electronics and IT (MeitY). [2]

- India is amongst the fastest growing fintech markets in the world and there are 6,636 finTech startups in India. [3]

- Indian fintech industry’s market size reached $50 Bn in 2021 and is estimated to reach ~$150 Bn by 2025-26. [3]

- As of June 2022, India has 23 fintech companies, which have gained ‘Unicorn Status’.[3]

- Nowadays, most of the fintech Startups are working in ‘Payments’ with the most popular point of access being smartphones (66%) which are available 24×7. [4]

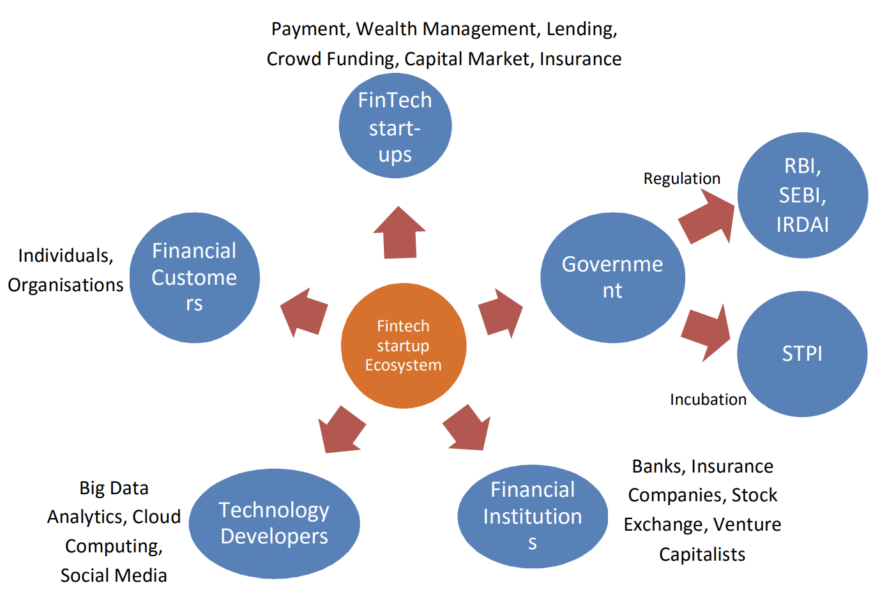

2. Why we need to regulate Fintech start-ups?

As mentioned above, with boost and support from Government of India, fintech companies are rapidly diversifying themselves in the market. They are working in retail payments, share market, mutual funds, insurance etc. They keep on launching their new products or apps in the market directly. However, it is not known whether a fintech software product launched in the market is safe or not. For example one fintech company launches a product or an app and one customer install that product. He/she links his/her bank account to that software product. Later, he/she came to know that his/her bank account is empty as it was a fraud due to some bug or hacking of account. Installing untested or unverified fintech app or product is a risky preposition. Hence, appropriate test checks in fintech products are quite important.

To safeguard customer and prevent them from falling into the prey of such frauds, Reserve Bank of India (RBI) has launched Regulatory Sandbox (RS). RS provides check or controlled environment to all the fintech products or apps so that they could be tested and declared safe before launching it into the market. [5]

RBI announced fourth Cohort on the theme “Prevention and Mitigation of Financial Frauds” as the frauds will be prevented by emerging technologies. Algorithms will be made in AI/ML to prevent or mitigate financial frauds. This shall safeguard the customer as well as saving Fintech start-ups’ time and cost. The sandbox approach provides a safe and conducive environment to experiment with innovative approaches (including FinTech solutions), and where the consequences of failure, if any, can be contained.[5] The regulations are aimed at maintaining a balance between the development of the financial sector through IT while keeping in view the policies & terms regarding money transactions.

A combination of emerging technologies like Artificial Intelligence, Machine learning, Internet of Things etc. with innovation have shown tremendous potential for sustainable development and growth of smart solutions. Indian tech-startups are already developing niche products to take advantage of the huge potential created through these emerging technologies.

In case of any concern arises during the sandbox period, appropriate modifications can be made before the product is launched in the market. Financial Domain included in the RS are money transfer services, digital know-your customer, financial inclusions and cyber security products are included but crypto-currency, credit registry, and credit information are left out.[5]

3. Government of India ‘push’ in promoting Digital Payments and Fintech startups

For adoption of these technologies by Indian citizens, Government of India launched BHIM-UPI app (on 30th Dec 2016) and Rupay debit cards (26th Mar, 2012) for promoting digital payments with zero processing fees (Merchant Discount Rate (MDR) was made zero in Jan 2020). Consequently, BHIMUPI (Bharat Interface for Money – Unified Payment Interface) has attracted customers exponentially wherein customers were also given cashback. This was an attempt by the Government of India to make more and more people ‘digital’. Further, the Government has taken various initiatives to promote digital payments and in order to safeguard Indian fintech companies, MeitY announced ‘Incentive Schemes for promotion of Rupay Debit Cards and low-value BHIM-UPI transactions (P2M) to safeguard transaction value up to Rs. 2000’. [7] Consequently, this led to exponential growth at rate of 33% (YoY) in digital transactions.[2] The pandemic has highlighted that digital payments enable safety for citizens through contactless modes of payments as well as provide impetus to economy. Hence, we can see that the roadmap of Government of India was quite clear. They want to make digital payments affordable, secure, transparent and accessible to all citizens. During FY 2020-21, more than 40% financial transactions were digital transactions and this is projected to increase be three-fold by FY 2025-26. [6] For safe and secure digital transactions, we need quality financial software products. The technology integration of banking services brought out the paradigm shift in banking sector. Now, there is no need to go to the bank for simple money transactions. A person living in remote areas or villages where there is no bank or post office can transfer money to person living in anywhere through mobile banking or vice versa.

If you are using apps like Paytm/GooglePay for paying your taxi fare or restaurant bill, then, you are already a part of this fintech startup ecosystem! This system has actually eradicated our need to keep cash. As these services are online, they have brought transparency to the banking system. We are witnessing visible changes in banking landscape. All this is possible today because of many Government initiatives & regulations as well as innovative fintech companies’ products.

4. Why Fintech start-ups need incubators/accelerators like STPI FinBlue?

Start-ups working in fintech space need proper platform to nurture their idea. Software Technology Parks of India in consultation with Ministry of Electronics & IT (MeitY) has launched various Centers of Entrepreneurship (CoEs). To build the next wave of promising fintech start-ups, STPI Center of Entrepreneurship (CoE) in the fintech space was operationalized at STPI Chennai in 2019. FinBlue CoE has been established in partnership with MeitY, State Govt., IIT Chennai, TiE Chennai and various industry partners such as Intellect Design, NPCI, Yes Bank, Paypal, Pontaq Ventures, RBS, Torus Innovations etc. to provide complete handholding and support to start-ups. It offers an integrated program to Start-ups to scale through its 100 plug-and-play seater incubation facility by providing access to the SandBox environment which consists of APIs of different participating banks, NPCI products, Core Banking Software and other enabling services through various stakeholders.[8]

FinBlue aims to support 58 start-ups over the period of 5 years with special focus on areas like Trading, Banking, Lending, Remittances, Insurance, Risk & Compliance, Wealth Management, Financial Inclusions etc. [8]

5. Advantage STPI

The aim of STPI FinBlue (CoE) is to help fintech startups reach an inflection point moving from the ideation stage to business stage in the most effective and efficient manner. This helps startups to become scalable and sustainable with solid business models. STPI CoE functions as a single-window facilitation center with an aim to provide structural and fundamental support including Lab & incubation, training, mentoring, hand-holding, access to funds, networking, market connect etc. It is a collaborative model among Govt. of India, State Govt., Industry, Academia, & Technology Experts, Venture Capitalists etc. This collaborative model of the CoEs is further extended with an eminent industry/academia/entrepreneur on boarded as “Chief Mentor” who also act as the brand

ambassador of the CoE.[8] In addition to this, STPI provides access to global marketing partners as well as participation in global events which act as a boon for exponential growth of startups. [9]

If the startup is already having minimum viable product with patronizing customers and is looking to quickly grow their business then accelerator program would be the right option. However, if your fintech startup is under the ideation stage where you need support regarding flushing out products or services as well as guidance with management structure then fintech Incubators works better.

STPI Finblue has launched NGIS 4.0 under the theme “Transforming Digital India by developing innovative solutions using emerging technologies in Banking & Financial Sector”. Through this article, STPI is inviting students, scholars and startups to take up the challenge of STPI. They can apply by visiting this link- https://innovate.stpinext.in. STPI is looking forward to their enthusiastic participation for availing NGIS seed fund of up to Rs.25 lakhs and other key takeaways. Apply Now!

[10]

6. Technology and Financial Services

With the vision to make India – cashless economy, it is pertinent to magnify the role of fintech startups. However, there is a still major chunk of our population who are still deprived of banking services. They are still dependent on landlords or middlemen for loans or any other financial help at very high interest rates. The fintech sector can provide them with much needed assistance. Even for MSME sector, lack of working capital and access to credit are making them stagnant. As a result, they are on the verge of closure. The fintech sector can actually channelize help for them regarding arranging capital. Based on their credit score – a platform can be developed by fintech startups, MSME sector will be able to get financial help at easy interests. Moreover, these start-ups can bring transparency to lending business.

7. Challenges Ahead

- Databases constituted by RBI/NPCI should be shared with start-ups.

- Digitization and office automation has made the information available in these systems more lucrative to cyber attackers. Cyber thefts on databases of debit card companies as well as banks which can cause personal as well as financial damage to major clients. These cyber attackers can misuse this information. The major risk related to fintech domain is ensuring data protection and data security.

- Money laundering is also one of the major challenges.

- For fintech software products to work seamlessly, Internet connectivity should be stable. There should not be any fluctuation in the signal when the transaction is under process.

- Moreover, AI/ML is used to build algorithms for fintech software apps. This algorithm should not go in an infinite loop or out of control under any circumstances.

8. The Way Forward

As these apps contain personal as well as financial data of all citizens, it is necessary to make foolproof arrangements regarding data protection and data security of such sensitive information. Government of India has already taken necessary steps to develop cyber security software products rather than depending on imports. MeitY has already started ‘Cyber Jagrookhta Diwas’ to educate and spread awareness to the masses.

Frauds in digital payments have increased exponentially with the increase in digital transactions. In order to mitigate these frauds, it is imperative to regulate these financial innovations.

Small businesses usually fail as they lack required support. In consultation with MeitY, STPI is successfully doing this by providing a holistic Fintech ecosystem that covers the entire needful support that budding startups need initially. STPI FinBlue offers an integrated program for start-ups to scale up through its incubation facility. As India prepares for its economic leap, it is important for all relevant stakeholders like Government including RBI/SEBI/IRDAI, industry bodies and entrepreneurs to come together to plug the gaps and help in hand-holding fintech startups to realize their true potential.

Our Hon’ble Prime Minister of India has said that “I dream of Digital India where 1.3 billion connected Indians drive innovation & Government services are easily and efficiently available to citizens on Mobile devices”.

In order to realize his dream, Digital transformation is only possible when our future banks should become completely ‘Digital’. The adoption of innovative use of technology can enable digital banks to understand the needs of low-income clients and so offer them appropriate financial services at low cost in a transparent and secure manner. However, the distinction between traditional banks and digital banks should fade away soon and the same regulatory approach should be followed for both banks to serve all customers at par.

References

[1]. NITI Aayog Report on Fintech Conclave 2019

[2]. Livemint – “India made 7,422 crores digital payments in FY22 at 33% growth rate – MeitY” on Mar 23, 2022

[3] Invest India – “India – A global Fintech Superpower” on Jul 04, 2022

[4]. Statista – “Digital payments in India” on Apr 26, 2022

[5].“Enabling Framework for Regulatory Sandbox” by FinTech Division, RBI on Oct. 8, 2021

[6]. Outlook India.com – RBI Payments Vision 2025 Aims 3-fold Increase In Digital Payments on 17, June 2022

[7]. MeitY notification no. 24(1)/2020-DPD-Part(2) dt. 17.12.2021 entitled “Incentive Schemes for promotion of Rupay Debit Cards and low-value BHIM-UPI transactions (P2M)”

[8]. STPI Annual Report 2020-21

[9]. STPI FinBlue

[10]. STPINEXT

{kind=link}